Are Target Maturity Funds An Alternative To Bank FDs?

Fixed deposits are one of the oldest investment options that are considered safe, assured, and stable. Currently, on account of the rising inflation, the central bank of India has increased the repo rate quite a few times. As on 8th February 2023, the repo rate was escalated to 6.50%. While this has increased the burden of loan holders, it improved the interest rates received by bank fixed...

5 Personal finance trends to consider in 2023

The Indian economy being in its developing phase frequently provides the platform to introduce new and innovative avenues in the finance sector. Over the past few years, we have witnessed growth at an exponential rate after the commerce space was met with digitalization. Subsequently, it opened up the means to explore new-age and advanced methods of managing one’s personal finance. As we...

P2P Lending Decoded

How do banks make money? Simple, when you deposit your money with a bank, they further lend it to borrowers at a higher interest rate compared to the rate you get as the interest on your deposits. And that margin between the interest earned by lending and the interest paid on deposits is the profit for banks. For example, you deposit a certain amount of money with a bank at a 5% rate...

7 Key Differences Between UPI and e-RUPI

In the constant progress towards expanding the ‘Digital India’ movement, the government of India is also focusing extensively on digitizing the economic aspects. From introducing digital banking facilities to popularizing the UPI payment system, the steps taken by the Indian government to revolutionize the Indian economy have received an overwhelming response from people across the...

Things To Do At The Start Of The Financial Year

Now that we are in the month of April, and the new financial year has started. It is an excellent time to review your finances. In this blog, we will see what things should be there on your to-do list for this month. 1. Increase Monthly Investment – Increase your saving and investment amount to improve your financial health. As per the financial experts, you must maintain at least a...

Union Budget 2022 Highlights – Economy, Digital assets, Infrastructure and more

Amidst the unpredictable COVID scenario, difficult past and an anxious future, Finance Minister Nirmala Sitharaman presented the much-awaited and extremely hopeful Union Budget for the financial year 2022 – 2023, today i.e. 1st February 2022. Presented for approx. one hour and thirty minutes, the duration of the Budget presentation seemed extremely short compared to the long list of...

The Four Pillars of Personal Finance

“The Journey of a thousand miles must begin with a single step” – Lao Tzu. The single step of analyzing your four pillars will help to provide you with a framework to manage money. Managing money has become the need of the hour. Today youngsters find this as the most difficult task unlike earlier. Irrespective of our income, age, wealth, investment, credit card bill, and other...

Wealth Habits – Learn, Unlearn and Relearn

When the entire world was upgrading its defence technology in preparation for a World War III or asimilar situation between neighbouring countries, no one taught us that World War III would befought with social distancing, wearing a double mask and getting vaccinated against COVID. Lessonlearnt “Human discipline is more important and critical than any technology to discipline...

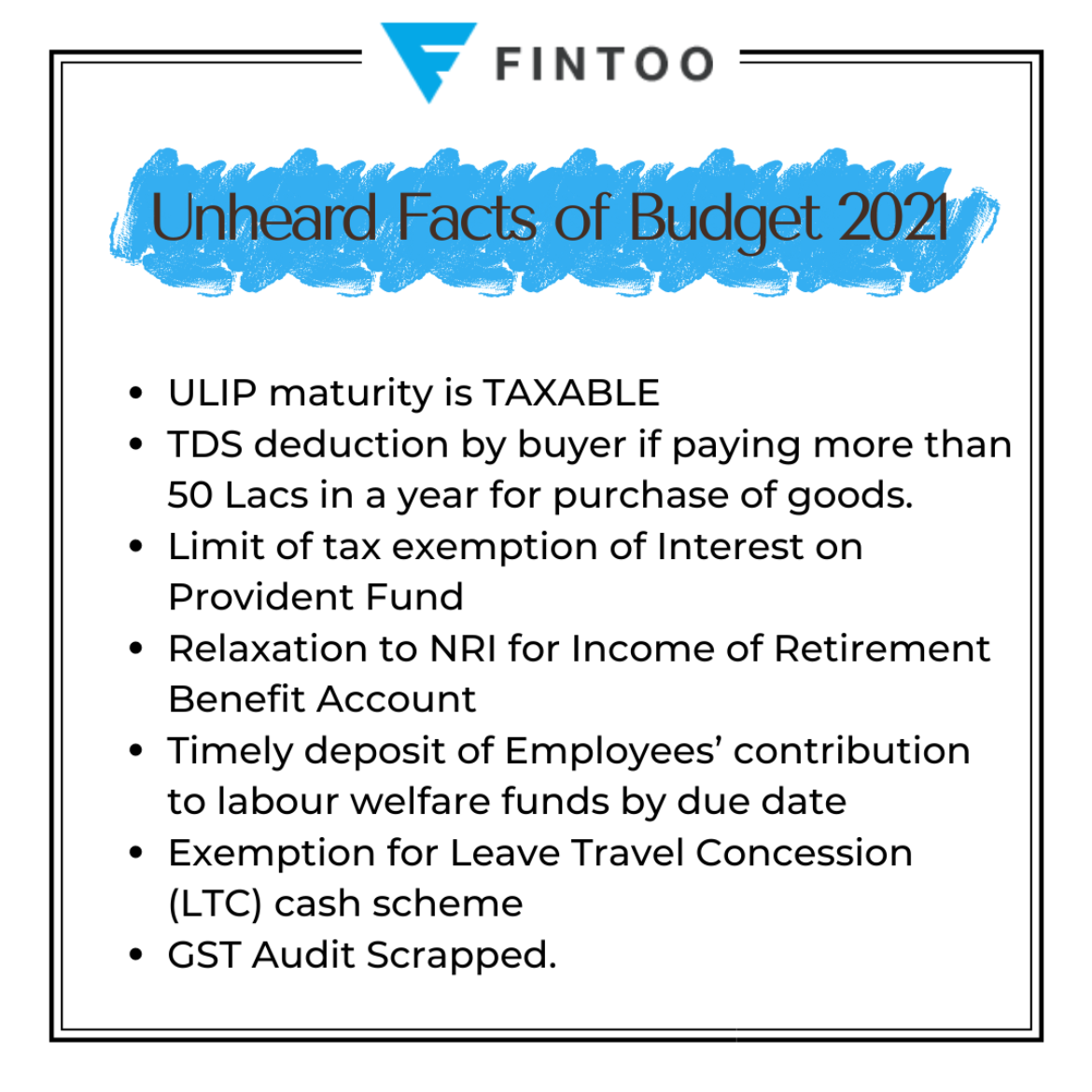

Unheard Facts of Budget 2021

Some of the facts which you don’t know about Budget 21. Here is the list 1. ULIP maturity is TAXABLE. Budget 2021 has proposed not to provide tax exemption under section 10(10D) of Income Tax Act for maturity proceeds of the unit-linked insurance policies (Ulips) with annual premium above ₹2.5 lakh. The rules will apply for Ulips issued on or after 1 February 2021. According to...