India–US Trade Talks: Impact on Economic Growth and Economic Development

Introduction: Why Global Trade Talks Matter for India Trade negotiations between India and the U.S. are back in the headlines, with new political momentum and renewed investor attention. Former U.S. President Donald Trump’s recent remarks about pursuing a trade deal with India stirred interest across markets and policy circles. But while the rhetoric is loud, the progress behind the scenes...

How to Safeguard Your Digital Wealth

Why cybersecurity is the new cornerstone of wealth protection in 2025 The way we understand, grow, and store wealth has transformed drastically. Once confined to paper certificates, vaults, and real estate deeds, wealth today lives in the cloud, in digital wallets, on investment platforms, and across financial apps. But with this evolution comes a sobering reality: your digital wealth is...Systematic Transfer Plan (STP): The Key to Growing Your Wealth Smartly

Introduction: The Investment Dilemma Imagine you’ve just received a hefty bonus or sold a property, and now you’re pondering: “Should I invest this lump sum in the stock market?” The market’s volatility makes you hesitant. Enter the Systematic Transfer Plan (STP), a strategy that allows you to transfer funds from a debt to an equity mutual fund in a staggered...

Indian Stock Market in 2025: A Global Rollercoaster

2025 hasn’t been kind to the Indian stock market. From sudden dips to investor panic, a cocktail of global influences has turned the market into a rollercoaster. But if you’re wondering why this is happening—and more importantly, what you should do—you’re in the right place. Let’s break down the chaos and bring some clarity. Market Mayhem: What’s Happening? The Sensex fell by...

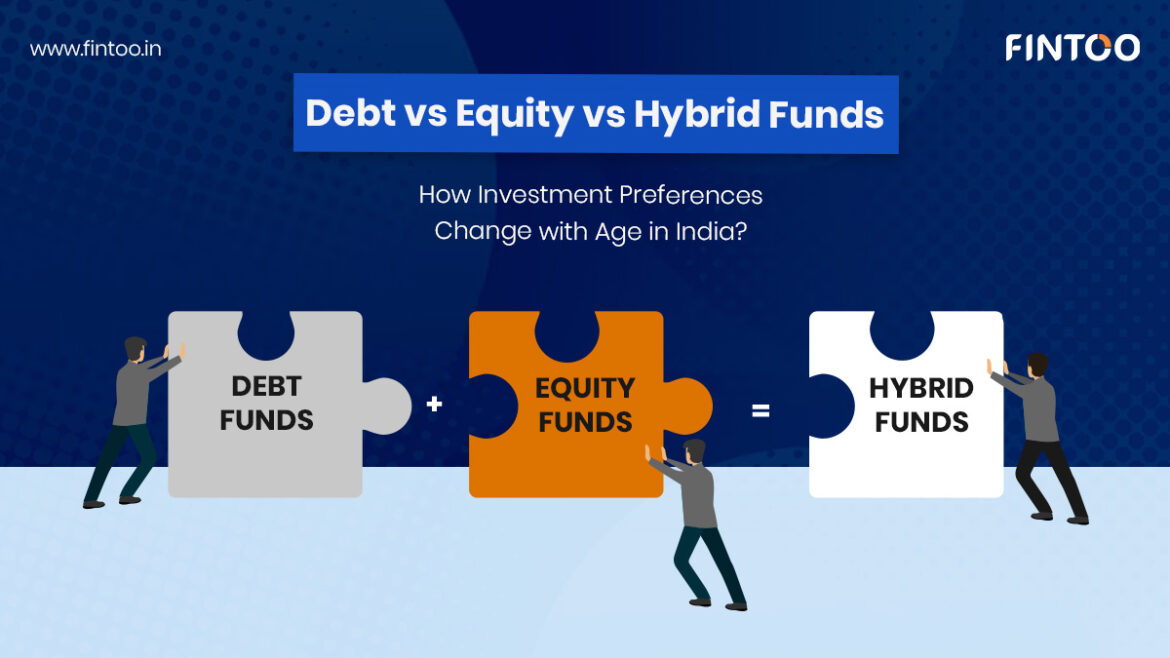

Debt vs Equity vs Hybrid Funds: How Investment Preferences Change with Age in India

When it comes to investing, one size never fits all. In India’s dynamic financial ecosystem, age plays a massive role in shaping how people choose to grow and protect their money. And it’s not just a hunch — it’s backed by data. A joint report by AMFI and Crisil Intelligence offers fascinating insight into how mutual fund preferences evolve with age. It turns out, we’re not just getting older...

Refiring, Not Retiring: A Purposeful Approach to Retirement for Indian Investors

Let’s be honest — for most of us growing up in India, retirement always meant one thing: you work hard your whole life, raise a family, pay off your loans, and finally settle down into a slower pace of life. Maybe you move to your hometown, maybe you spend time with grandkids. The goal? To live off your savings and just “take it easy.” But that picture is changing. Rapidly. Today,...

Gold’s Glorious Run in 2025: What Indian Investors Must Know

Gold has always held a special place in the Indian heart and home. From weddings to Diwali to the arrival of a newborn, gold isn’t just bought, it’s celebrated. But in 2025, gold is doing more than just adorning our wrists and necks. It’s making headlines in the investment world — and for all the right reasons. At Fintoo, we’ve seen a sharp rise in conversations around gold. And the...

Best Government Investment Schemes to Invest in 2025

Looking for a smart way to grow your hard-earned money while keeping it secure? Government-backed investment schemes in India might just be what you need. They offer the perfect mix of guaranteed returns, flexibility, and long-term security—making them ideal for all financial goals, whether saving for retirement, a child’s education, or just building wealth. What’s great about...

ETFs: All You Need To Know About Exchange Traded Funds

ETFs are a sound investment plan, offering a cost-effective avenue to participate in the stock market, providing exposure without the burden of high expenses. Listed on exchanges and traded similarly to stocks, they provide liquidity and real-time settlement. Notably low-risk, ETFs replicate stock indices, presenting a diversified investment approach, in contrast to concentrating on a...