Tax Declaration Guide For Salaried Employees

Navigating income tax and declarations can be complex. In this blog, Fintoo – your partner in optimizing fiscal decisions – has simplified Income Tax Declaration (ITD); from understanding Form 12BB to strategic tax savings. Read on to discover how to make tax planning savvy and rewarding! Essential Guide to Income Tax Declaration – ITD An income Tax Declaration (ITD) is a crucial...

How to File ITR 2 online FY 2022-23?

The Income Tax Department has issued 7 different types of ITR forms to categorise taxpayers based on their source of income, residential status, and a few other factors. Let us understand the eligibility of filing ITR 2 and how to file it online. Who can file ITR 2? The ITR 2 is a form that can be filed by individuals and HUFs who are Residents (ROR/RNOR) or non-residents earning income...

Common Mistakes to Avoid while filing ITR

As the ITR filing due date is almost nearing, many taxpayers are hurrying to file their ITRs. While it is crucial to get your ITR filed before 31st July 2023, it is also essential to ensure you don’t rush into it. Usually, individual taxpayers prefer handling their tax filing on their own. So, complications in understanding the tax laws and the last-minute filing pressure can cause taxpayers...

How To File ITR-1 SAHAJ Online In FY 2022-23?

Are you feeling overwhelmed by the process of filing your income tax return? Let go of your tax-related worries, as we provide a hassle-free solution for filing. The ITR-1, commonly known as Sahaj Form, is now available to cater to individuals with an income of up to Rs—50 lakh. What Is ITR-1 SAHAJ (Income Tax Return (ITR) Form-1) Taxpayers and individuals who are residents...

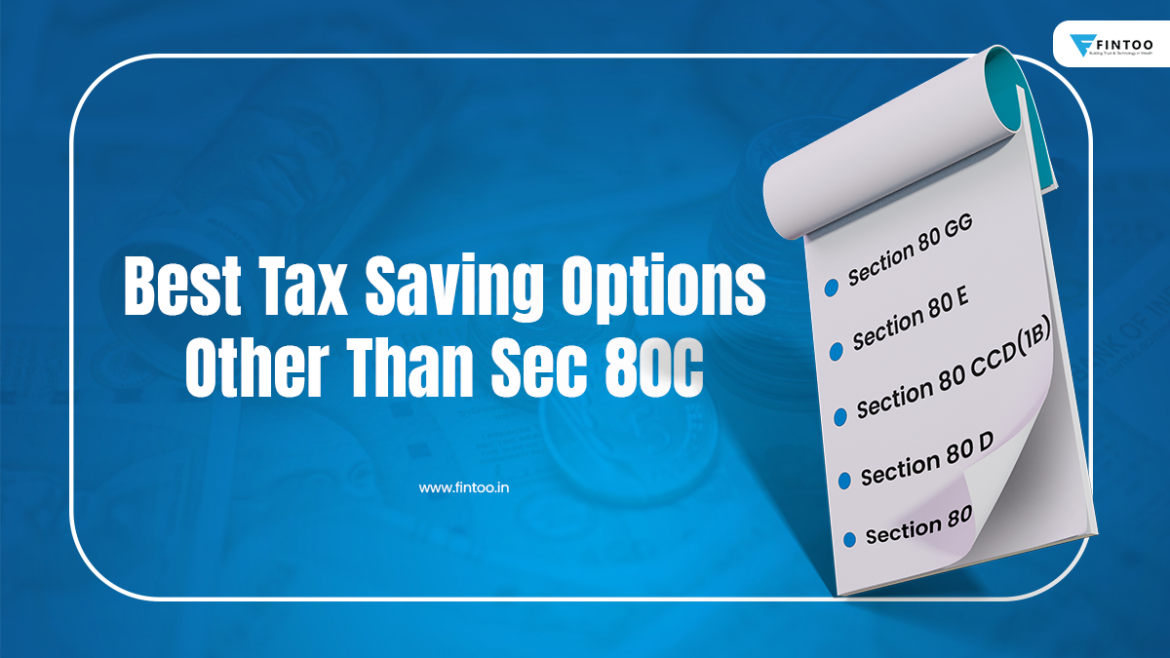

Best Tax Saving Investment Options Other Than Section 80C

When it comes to saving taxes, most taxpayers are already aware of the common deductions available under Section 80C of the Income Tax Act, such as ELSS, PPF, NPS, Home Loan Interest, or HRA. But apart from these, there are several lesser-known tax saving options that can further maximize your savings by reducing your tax liability. In this blog, we will discuss top tax saving...

Documents Required to File Your Income Tax Return (ITR)

Filing an income tax return (ITR) accurately and on time is an essential obligation for taxpayers. Just like every person’s source is income, income structure, and tax liability are different, and the documents required for filing their ITR are also different. While we obviously cannot expect everyone to know about the technical and complicated process of ITR filing, we believe that every...

Decoding Major Deductions Under Old Tax Regime

As per the data, more than 2 crore taxpayers in the age group of 18 to 35 years filed their Income Tax Returns (ITRs) in FY 2022-23. In the Budget 2023, the Central Government announced that annual income of up to Rs. 7 lakhs would be tax-free under the New Tax Regime. This is along with the standard deduction of Rs. 50,000/- under the New Regime, which will make income up to Rs. 7.5...

ITR 1 FILING PROCESS

Registered users of the e-Filing portal can pre-fill and submit their ITR-1 forms. Individual taxpayers can use this service to file ITR-1 online via the e-Filing portal and by gaining access to the offline tool. This user guide describes the ITR-1 online filing procedure. To File online visit the https://www.incometax.gov.in/IEC/FOPORTAL website. Registered users with valid USER ID and...

ITR 2 FILING PROCESS

Registered users of the e-Filing portal can pre-fill and submit their ITR-2 forms. Individual taxpayers can use this service to file ITR-1 online via the e-Filing portal and by gaining access to the offline tool. This user guide describes the ITR-1 online filing procedure. To File online visit the https://www.incometax.gov.in/IEC/FOPORTAL website. Registered users with valid USER ID and...