Calculating Mutual fund Returns – CAGR, XIRR and Absolute Returns

Returns are a major reason why any investor would want to invest in a scheme. But these returns depend on various factors. For example, when it comes to mutual funds, the returns generated by a fund are based on the performance of the underlying asset, the expense ratio, market conditions, etc. Let’s say you are getting a mutual fund return of 13% over the past three years,...

Will Taxing High-Value Insurance Benefit Debt Mutual Funds?

Life insurance has always been a preferred investment option for all people due to the financial security it offers to a family after the demise of the policyholder. It also becomes ideal for people with a conservative risk profile. In the budget 2023, it was announced that high-value insurance purchases would henceforth be taxed with effect from 1st April 2023. This newly introduced...

Your Guide To Investing In Passive Mutual Funds

Mutual funds are an exceptional market-linked investment opportunity available at present, offering adequate risk diversification and the potential for significant long-term returns. However, selecting the right mutual fund can take time and effort, considering the range of options available in the market. To make the right investment decision, it is crucial to differentiate between the...

Star Rating Methodology Of Mutual Funds

Mutual Fund star rating methodology is a measure of its performance with respect to the returns, risk, and the fund’s capacity to generate returns at a particular level of risk. This rating system primarily focuses on comparing the performance of the fund within its category. Apart from the comparison, factors like Date of inception, YTM, Expense ratio, etc. also play a vital role in...

Understanding Indexation In Debt Mutual Funds

Attributing to the rise in inflation, it has become a requisite to have sufficient investments in order to meet your needs. With inflation causing a ruckus in the global economy, investors have begun expanding their orbit and stepping into non-traditional investments to keep up with the pace of rising expenses. Among various channels that provide returns adapting to the rate of inflation, you...

How To Select The Best Debt Mutual Funds?

While commuting to work, you catch a glimpse of the same billboard every morning. It says something along the same lines of ‘Get rid of all your financial worries by investing in best debt mutual funds.’ You might find it amusing. If it were that easy, wouldn’t everyone be rich? But what if we told you, it is not that hard or out of reach either? Because with every little eye roll or...

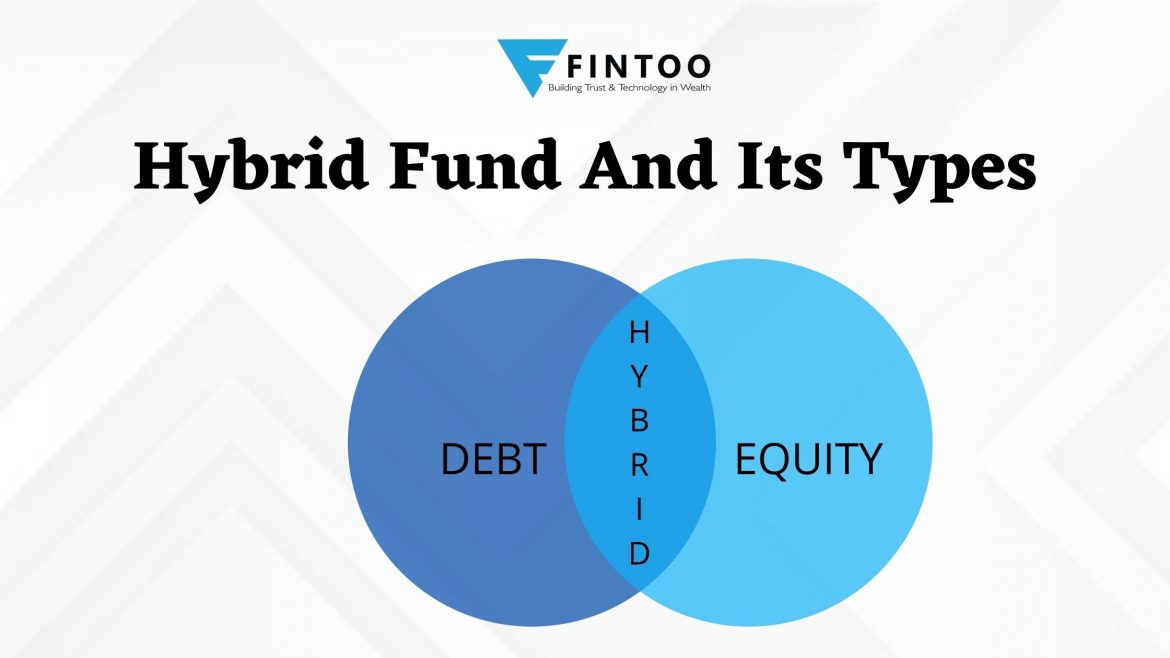

Hybrid Funds And Its Types

“Mutual funds are subject to market risk, you should read all scheme related documents carefully before investing” this is something which we all have memorized unknowingly, isn’t it? So, as they say, ‘where there is an investment, there is a risk.’ And every investor has a different risk-taking capacity. While some investors prefer to take a high risk to get high returns, some happily...

How ELSS is better than any other Tax saving scheme?

If you are looking for tax savings this season, then look no more. We have come up with an interesting blog on the evergreen topic of whether ELSS is better than any other tax-saving scheme. And what’s more interesting is that we have also summed up answers to every Why of yours. So what are you waiting for? Let’s skip this journey to the main content. What options do you have for tax...

What is ELSS? Is ELSS Different from Mutual Funds?

Mutual funds have revolutionized the way people invest. Earlier, risk-averse individuals preferred fixed deposits while risk-taking investors went for stock markets. However, lately, mutual funds are becoming a favourite among investors. They promise market-related returns while the risk is diversified over a wide portfolio. What’s more, even small investors can invest in a...